Have you seen what mortgage rates have been up to lately?

One day they drop a little. The next day, they bounce right back up.

If you’re trying to decide whether now’s the right time to buy a home, it’s understandable to feel a little unsure.

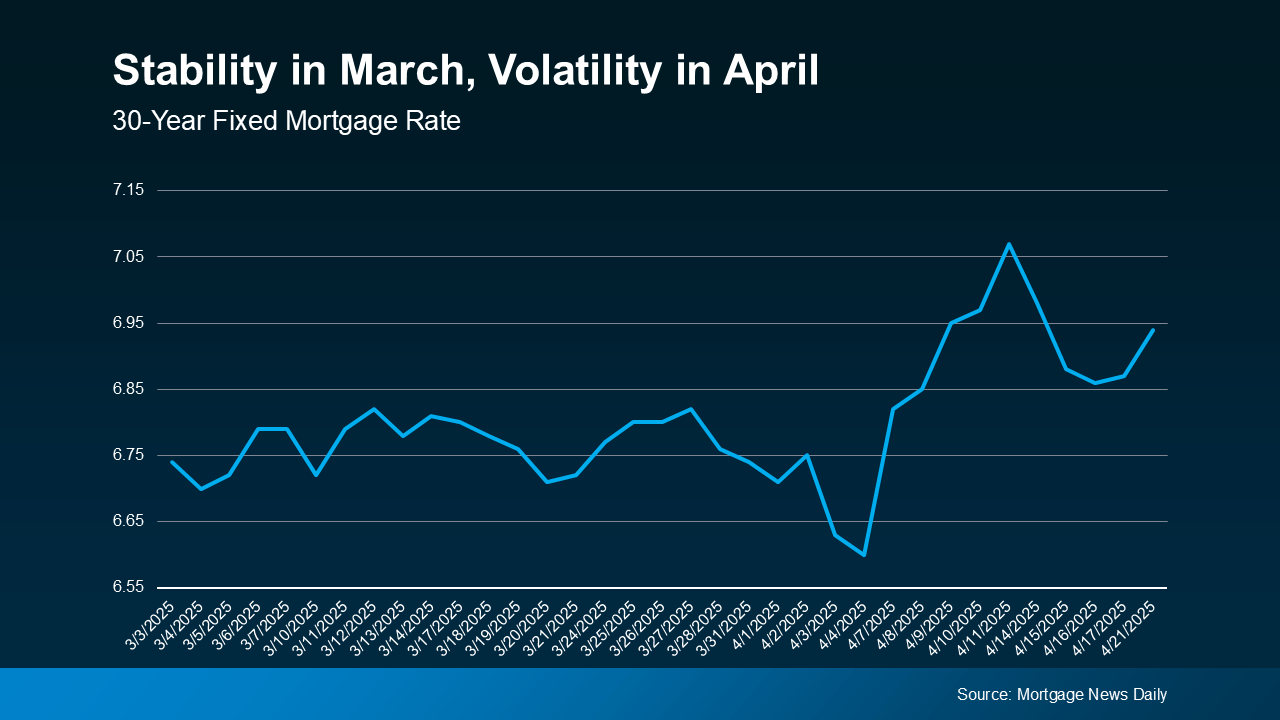

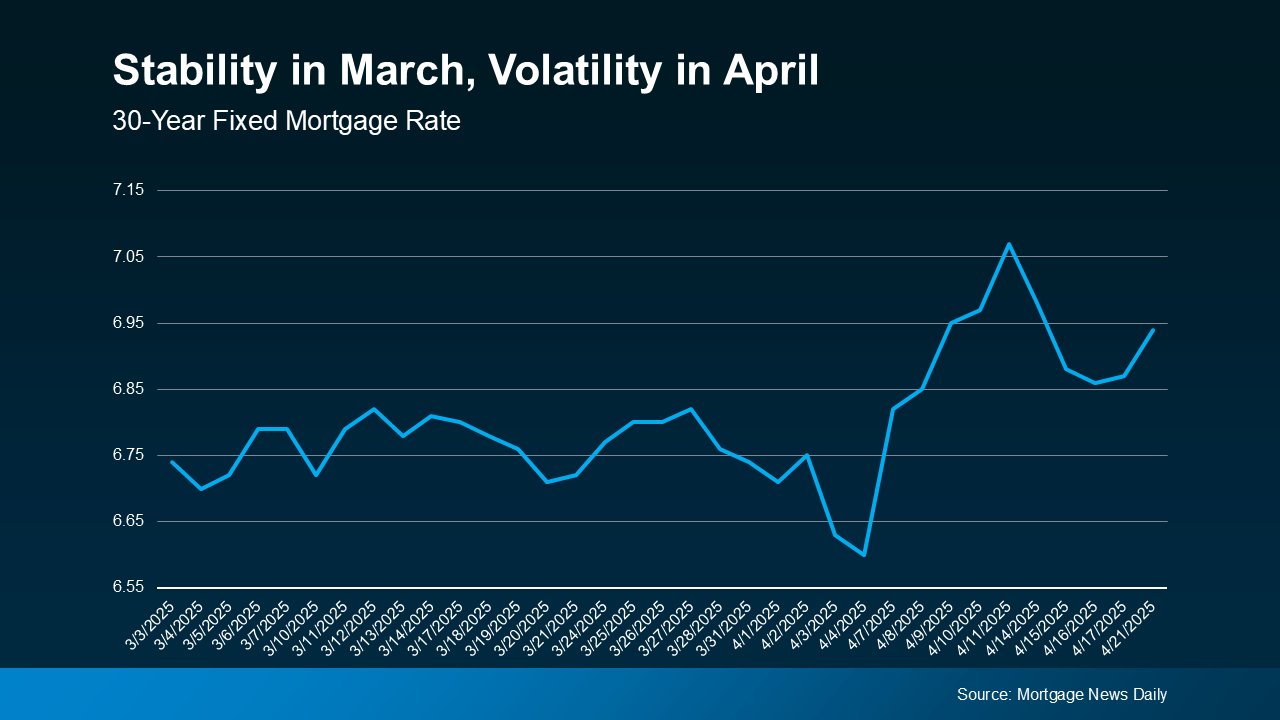

Let’s look at the facts. The graph below, based on data from Mortgage News Daily, shows what’s been happening with the 30-year fixed mortgage rate over the past several weeks.

📊 March brought some much-needed stability, but April has been a rollercoaster.

So what does this mean for you?

You Can’t Control the Market, but You Can Control Your Strategy

Here’s the truth: trying to “time the market” is rarely a winning game. Rates shift based on broader economic changes—many of which are out of your hands. The good news? You’re not powerless. You can take control of your financial readiness and work with experts to make the smartest move possible when you're ready.

Let’s break down the three things you can influence:

1. Your Credit Score

Your credit score plays a huge role in determining the mortgage rate you’ll qualify for. According to Bankrate:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage… Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

📌 Even a small boost to your score can lead to big savings on your monthly payment. If you're unsure about where you stand or how to improve, start by talking to a trustworthy loan officer who can help you build a roadmap.

2. Your Loan Type

Not all mortgage loans are created equal. As the Consumer Financial Protection Bureau (CFPB) explains:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans... Rates can be significantly different depending on what loan type you choose.”

Each loan type has unique qualifications and benefits. That’s why it’s important to speak with multiple lenders to understand your full range of options—and find what works best for your situation.

3. Your Loan Term

A mortgage isn’t just about the rate—it’s also about the term of your loan. Freddie Mac puts it this way:

“When choosing the right home loan for you, it’s important to consider the loan term... Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay.”

Whether you’re leaning toward a 15-, 20-, or 30-year loan, the right choice depends on your goals and timeline. A shorter term usually means a lower rate but higher monthly payments. Again—this is where your lender can help tailor your decision to your personal game plan.

The Bottom Line

You can’t control the economy. You can’t predict mortgage rate swings.

But you can put yourself in the strongest possible position—right now.

✔️ Know your credit score.

✔️ Understand your loan options.

✔️ Choose the loan term that fits your goals.

✔️ And above all—partner with professionals who will advocate for you every step of the way.

Let’s connect and talk about what you can do today to get ready for your next move—so that when the time is right, you’re ready to roll.