If you’re planning to buy a home this year, there’s one expense you can’t afford to overlook: closing costs.

Almost every buyer knows they exist, but not that many know exactly what they cover, or how much they can change depending on where you’re buying. Let’s break it down.

What Are Closing Costs?

Closing costs are the additional fees and payments you make when finalizing your home purchase. Every buyer pays them, and according to Freddie Mac, they typically include things like:

· Homeowner’s insurance

· Title insurance

· Loan application fees

· Credit report fees

· Loan origination fees

· Home appraisal

· Home inspection

· Property survey

· Attorney fees

Think of it as the “all the other stuff” bill that comes with your new set of house keys.

National vs. Local: Why They’re Different

You’ll often see a national estimate that closing costs run about 2% to 5% of the home price. That’s a helpful starting point for budgeting, but it doesn’t tell the full story.

Closing costs vary widely based on:

· State and local taxes (like transfer taxes and recording fees)

· Service costs for title, insurance, and attorney work in your market

· Local regulations and requirements

That’s why two buyers purchasing homes at the same price point in different states can end up paying thousands more or less at the closing table.

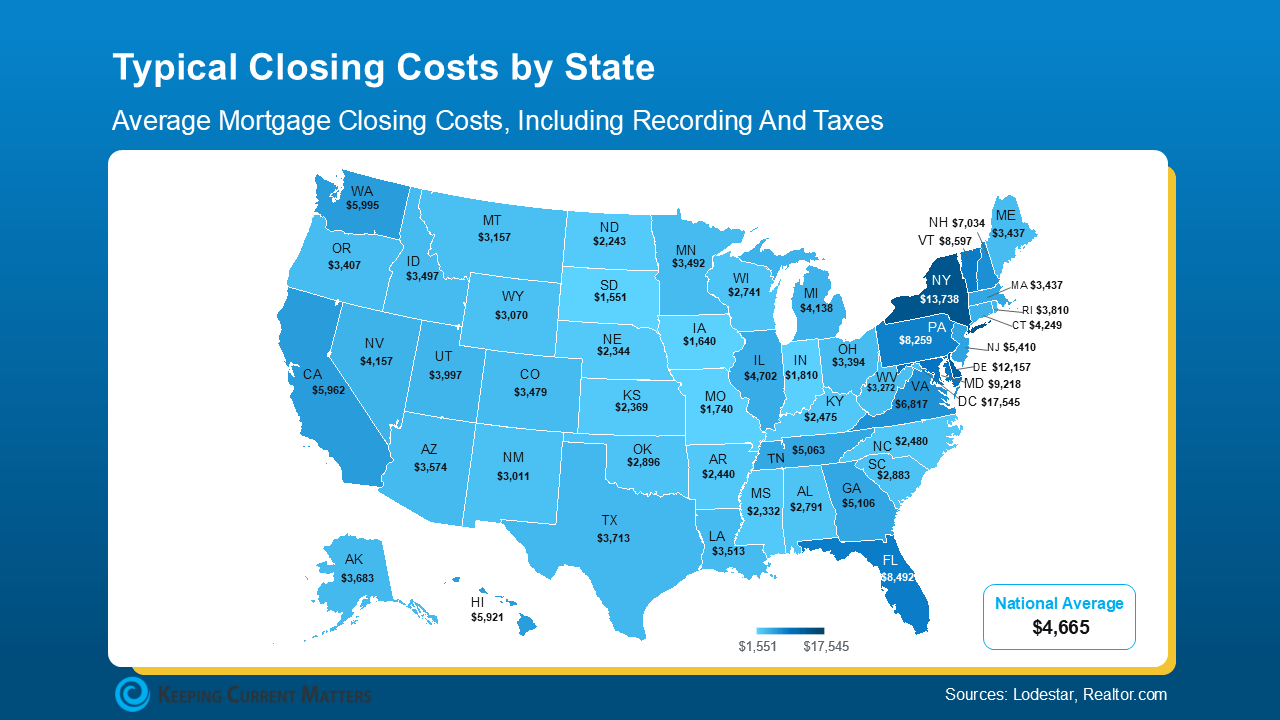

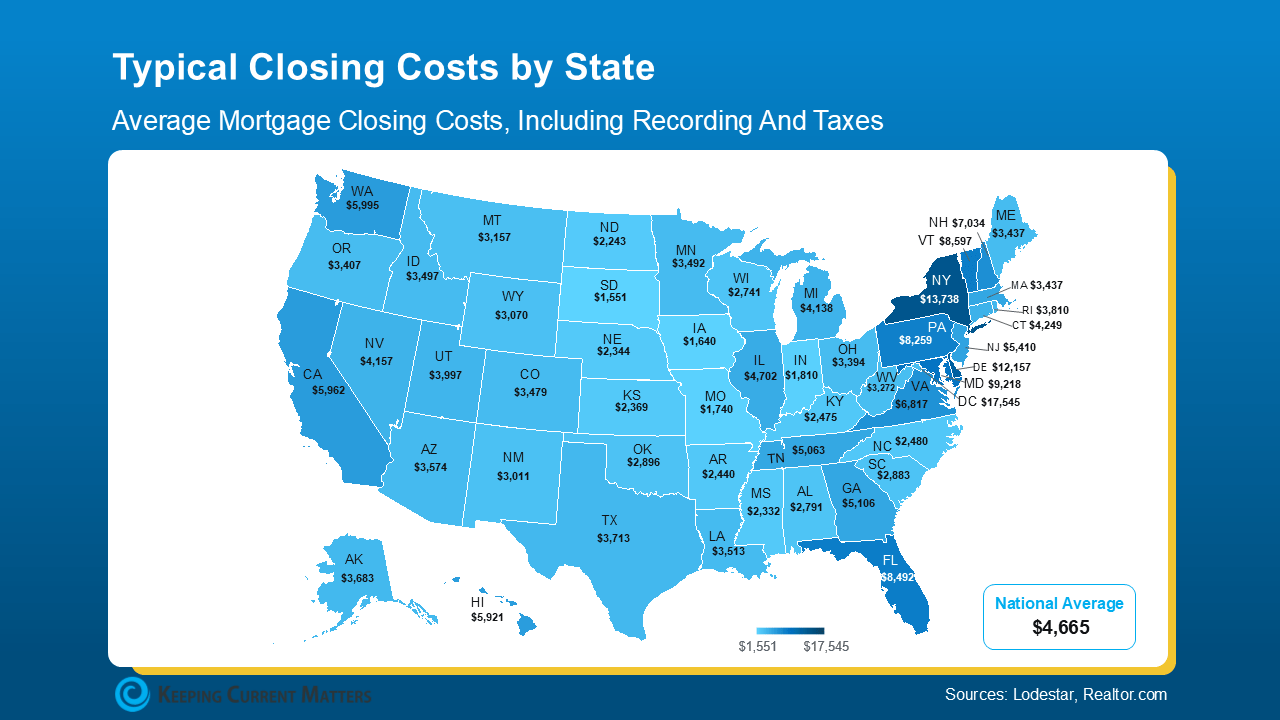

What the Numbers Look Like

The national average for closing costs sits at $4,665. But depending on your state, the number can swing dramatically.

· Some states hover around $1,500 to $3,000

· Others climb to $10,000 to $15,000

Here in Florida, the typical closing costs average around $8,490, which is almost double the national average. That’s why understanding the local picture matters—especially if you’re a first-time buyer.

Can You Reduce Your Closing Costs?

Yes. While some expenses are non-negotiable, you do have options to save. NerdWallet suggests:

· Negotiate with the seller – Ask for credits toward your closing costs as part of the contract.

· Shop around for insurance – Compare homeowner’s insurance quotes before you commit.

· Look into assistance programs – Some programs offer help based on location, profession, or first-time buyer status. Your lender and agent can connect you with resources.

Bottom Line

Closing costs are an unavoidable part of buying a home, but they don’t have to catch you by surprise. In Florida, where costs run higher than average, being prepared is half the battle.

If you’re thinking about buying in Tampa Bay, the smartest move you can make is connecting with a local agent and lender early. They’ll help you crunch the numbers for your budget and explore ways to keep your out-of-pocket costs manageable.

When you know what to expect, you walk into closing confident, not blindsided.

Annie & Kevin Rocks | Rocks Realty

Annie: 727-777-3264

Kevin: 727-389-6453